A reserve requirement of zero means they can loan out as much as they have on deposit + capital.

Nope, that'd be a full reserve requirement.

I'm afraid you're both wrong!

")

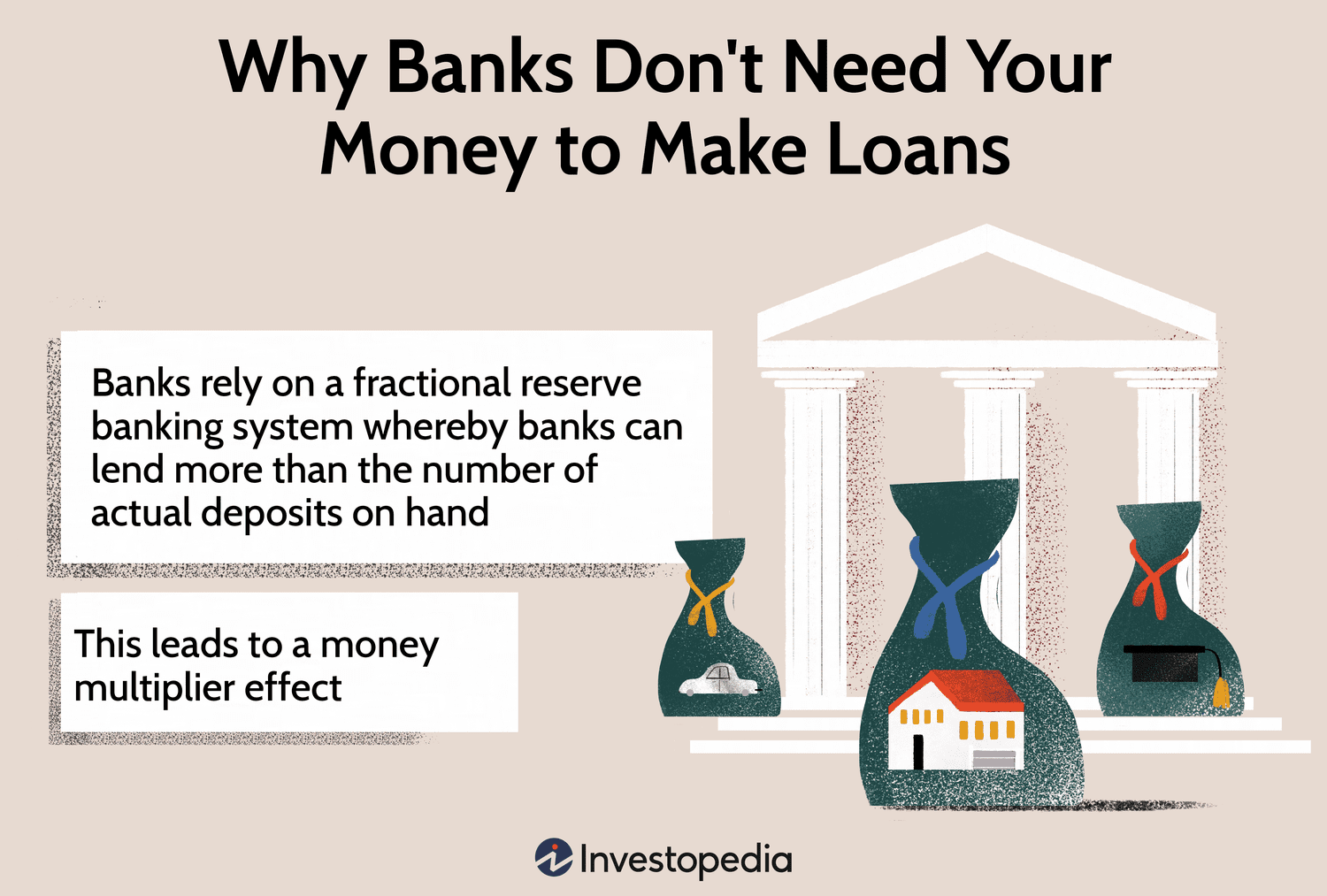

In particular, reserve requirement does NOT limit loans based on deposits; it limits deposits based on vault cash. In other words. deposits hinder meeting that requirement, rather than helping. (For brevity let's write "vault cash" to include the bank's deposits at a Federal Reserve Bank.)

A borrower — for definiteness say Jason borrows $1000 — will be given either cash or some sort of demand deposit paper. If he asks for cash, the bank cannot fulfill the loan unless they have $1000 in their vaults. This is true regardless of any reserve requirement,.

If instead the bank gives the borrower a checkbook with a $1000 balance, they now have $1000 on deposit, which is included in Loren's "as much as they have on deposit + capital." As long as the borrower accepts a checkbook, the loan could have been for a million dollars or a billion, regardless of how little capital the bank has! (There is a separate maximum on the liability-to-capital ratio independent of the reserve requirement, so a small bank couldn't do this.)

A 10% reserve requirement means that a bank with (demand) deposits totaling $70 million would have to have "MB" totaling at least $7 million. This MB would include the Federal Reserve notes the bank has in its vaults, and its demand deposits at Federal Reserve banks.

Loren Pechtel said:

Note that accounts receivable (the loan) is not money on deposit.

This seems confused. Deposits are liabilities. If the bank hasn't disposed of the cash customer deposited, that cash is "vault cash", not "money on deposit."

The whole question "Do banks 'create money' via loans or deposits?" seems like a red herring to me. Both the deposits and the loans are involved. But

(1) Deposits occur automatically. People don't like leaving large sums of cash under their mattress, while good loans may be hard to come by, depending on the economy. So it is the loans that are non-automatic, and therefore the essential key.

(2) When Bill deposits $1000 cash at a bank and receives a checkbook, "M1" (the definition of money supply) does NOT increase. Yes, the $1000 checkbook counts as money, but the $1000 the bank now has in its vault, while included in "MB" (see above), is NOT included in M1.

(3) It is when Jason then borrows $1000 from that bank that M1 increases by $1000. This is true whether he takes his $1000 as a checkbook or as cash from the bank's vault.

~ ~ ~ ~ ~ ~ ~ ~ ~

I still feel like finance has entered some sort of Fantasyland. Germany and Holland still have negative nominal interest rates on long-term "risk-free" debt? Absurd!! And the U.S. eliminating the reserve requirement baffles me.

Recall the 1980's when newly-deregulated Savings and Loans were making loans to cronies, loans that never got repaid? Is something like that soon to happen? What premiums do banks now pay to their FDIC insurer? I suppose in yet another gift to the banks, these premiums have been lowered also.

(I suppose the reason for that may be obvious. If the reserve req't is Zero, then 'Reserves' and 'Excess Reserves' become synonyms.)

(I suppose the reason for that may be obvious. If the reserve req't is Zero, then 'Reserves' and 'Excess Reserves' become synonyms.)